論説

この数年間、ほとんどの銀行は中小企業に対して画一的なサービスを提供してきた。多くの国で力強い経済成長が需要を加速し、思い切った決断をせずとも利益を出し続けることができる状況にあったからだ。しかし、決断を避けてきたことにより、結果的に多くの銀行は金融危機の後、非常に高い代償を払うこととなった。中小企業向け事業の利益は縮小し、巨額の貸し倒れを招き、厳しい規制が導入されることになったのだ。

多くの銀行は現在、中小企業に対して曖昧な対応をしている。例えば、米国の巨大銀行は10年前よりも小規模企業向けのローンを縮小している一方で、より高価な商品・サービスへの移行を強要している。英国の貸付市場は2009年から2013年にかけて毎年5%縮小していたが、2014年には2%拡大した。また、銀行は中小企業向け事業におけるデジタル化への投資を遅らせ、リテールバンキングと大企業向けビジネスに資源を集中させてもいる。

アジアやラテンアメリカの新興市場では、高い金利と比較的高額な手数料によって中小企業向け事業は利益率が非常に高く成り得るが、一部の銀行は困難に迫られている。超小規模企業に対して効率的に事業を行うためのビジネスモデルの構築や、中規模企業向けサービスをよりよいものにすることを怠ってきたため、顧客にそっぽを向かれ、成長の機会を失ってしまったのである。

銀行はデジタル化への投資を怠り、対抗する数々のテクノロジースタートアップ企業の台頭を許してしまった。決済(Alipay等)や貿易金融(Greensky)、融資(OnDeck)だけでなく、よりニッチな領域のスタートアップ企業も存在する。シンガポールのApexPeakは、小規模企業から受取手形を8割の金額で買い、月々3%の金利を受け取る「インボイスディスカウンティングモデル」という事業を行っている。同社では7営業日以内に取引を完了することができ、アジアやアフリカで2012年から現在までの間に7000取引を行ってきたという。これらのフィンテックは急速に既存の金融機関を脅かす規模にまで拡大してきた。

加えて、プライベートエクイティファンドや年金基金、保険会社も中規模企業への融資を拡大している。さらに小規模な企業に対してはブラジルのCielのようなアクワイアラーが受取手形を担保に積極的な融資を行っている。これら既存の銀行による融資の代替となるサービスは、少なくとも現時点では銀行規制の影響を受けないという点で優位である。

銀行がこれらの代替サービスに自行の顧客を奪われないようにしながら、同時に成長の機会を求めなければ、それは銀行がポートフォリオの一部を失うだけでなく、各国が自国経済にとって重要な中小企業セクターを失うことを意味するかもしれない。欧州では中小企業向け事業は銀行の収入の5~6割を占める巨大な収益源である。中小企業向け事業は多くのケイパビリティを必要とする複雑なビジネスではあるが、リテールバンキングよりも陳腐化しづらく、大企業向けのビジネスよりも顧客の価格感度が低い。加えて、中小企業の経済的な役割は非常に重要であり、欧州では雇用の3分の2を創出し、総付加価値の58%を占め、米国では従業員数500人以下の企業が全雇用の半数近くを創出している。

我々は銀行が中小企業に対して果たせる重要な役割を放棄せず、十分なリターンを得ることを諦めるべきではないと考えている。低いROEは決して改善不可能ではない。ROEの低さは主に高いデフォルト率とコストによるものであるが、もし銀行が業オペレーション改善によりROEをハードルレート以上にまで改善できたとするとどうだろうか。小規模企業向け事業において、モジュール化された商品・サービスと最大限デジタル化されたプロセスによりコストを大幅に下げ、中規模企業に対して高い水準で最適化されたサービスパッケージを提供し、さらにデータアナリティクスによりリスク査定のプロセスを改善できるモデルを構築できるとするとどうだろうか。ROEの観点から非常に魅力的なものになるはずだ。

実際、中小企業向けの事業は、最適化されたアプローチによって高い利益率を達成することが可能である。しかし多くの顧客をかかえながら資本コストをまかなうリターンを出しつつ、主力商品(決済口座と融資)のみから、健全な商品を創出することは難しい。銀行はクロスセルを促進するために、顧客のニーズを詳細に理解し、融資と付随的なサービス・商品の持続可能な組み合わせを考案する必要がある。また、それと同時に、事業主に対して、自行が便利で、早く、低コストなプロセスを提供できることを示さねばならない。

銀行は低金利、鈍い経済成長、厳しい規制、顧客の期待値の上昇といった多くの困難に直面している。小規模企業が便利でデジタル化されたサービスとより良い顧客体験を求める一方で、比較的大きな中規模企業は専門的なアドバイザリーや財務と会計を統合したシステムといったデジタル化されたソリューションを求めている。

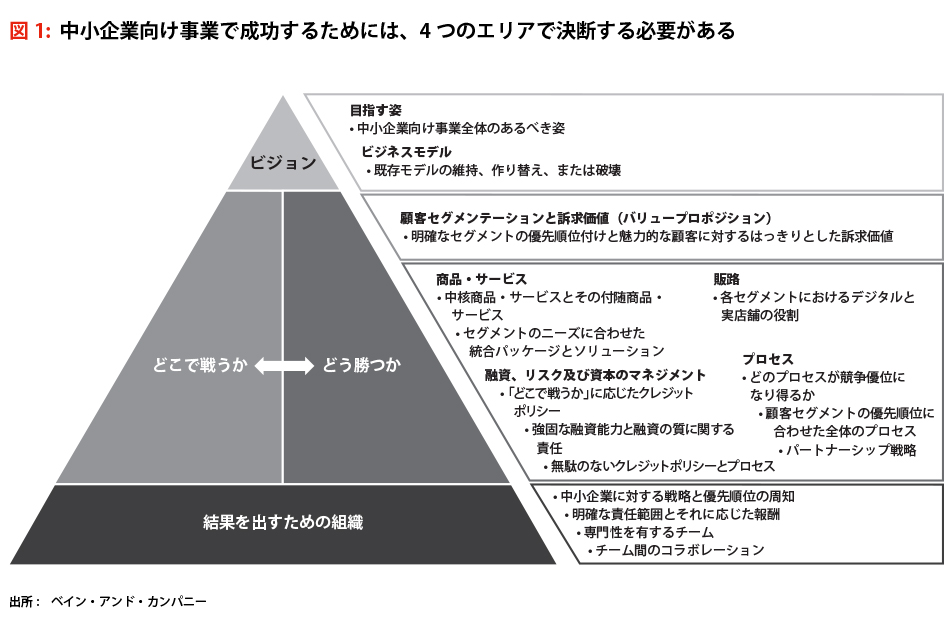

そのような状況の中で、これまでと似たような方法をとるのではなく、それぞれ根本的に違うと思われる選択肢の中から戦略的な選択を行うことで、中小向け事業を競争力のある形に変革させている銀行も存在する。その意思決定は4つの領域に分かれる(図1)。

- 中小企業向け事業における明確なビジョンの定義

- セグメンテーション、優先順位付け、訴求価値(バリュープロポジション)の定義による「どこで戦うか」の決断

- 商品、ソリューション、販路、プロセス、及び信用リスク管理などに対し、画期的なアプローチでなく、ターゲット市場で「どう勝つか」について熟慮されたアプローチの選択

- 変革のために組織を動かすこと

ビジョン

ビジョンの設定における本格的な選択は、2つの面にまたがっている。第一は、中小企業市場において、どの程度規模を拡大するのか、あるいは限定していくのか、である。拡大/限定という選択肢の他にも、現在のポジションから選択的に投資をするという選択肢や、究極的には撤退するという選択肢も存在する。

第二は、既存のビジネスモデルをどの程度維持/破壊するのか、である。銀行は、既存モデルの一要素を選択し、それらを改善させることが可能である。例えば新しい地域及びパートナーシップを加えること等によるモデルの刷新、既存の支店ネットワークをオンライン上に移すことによる既存モデルの破壊、などが考えられる。

銀行は一般的に現状維持を指向しがちで、中小企業向けビジネスモデルに関して大きな変革は行わず、最終的な利益創出のためにコスト削減に頼る傾向にある。しかし、10~20年間続けてきたこの方法でこれ以上の結果を望むことは難しい。利益の出る健全で持続的なビジネスモデルを構築するためには抜本的な改革が必要である。一つの考え方として、5年後のあるべき姿を定義してそこから逆算するという方法が有効である。そしてそれは現在の顧客セグメントや商品・サービス、及びチャネルのパターンを変えることに繋がるだろう。

ある欧州の銀行が中小企業向けビジネスを再度拡大するという決断をした事例では、事業全体を拡大しつつ、ヘルスケアやプロフェッショナルサービスといった特定の分野において市場シェアを倍以上にして首位獲得しようとしていた。その計画の第一段階では、ターゲット顧客のニーズに最適化した支店レベルでの対面アドバイザリーというニーズ対応への投資が大きくなるだろう。

どこで戦うか

ビジョンを明確にしてはじめて、ターゲットとする顧客、提供する商品、販路、及び訴求価値(バリュープロポジション)について適切な意思決定を行うことができる。そのためには以下の問いに答えなければならない。

- 顧客をどのようにセグメンテーションし、優先付けをするか

- 各セグメントに対する訴求価値は何か

市場の一部を獲得しようとするテクノロジー企業の攻撃に対して、広範囲の顧客セグメントに対してあらゆる商品・サービスを提供するという方法はますます脆弱になっている。そのような試みを続けていれば、高いコストと貸出に対する低いマージンに苦しむはめになる。

そのような苦境から抜け出すためには、熟慮された現実的な顧客セグメンテーションが必要である。いくつかの銀行は中小企業を業界や規模によってセグメンテーションし、場合によってはポートフォリオのコアとしていくつかのセグメントを定義しているが、セグメンテーションによる示唆に基づき、優先順位付けを行い、アクションに落と込んでいるのは一部の限られた銀行のみである。

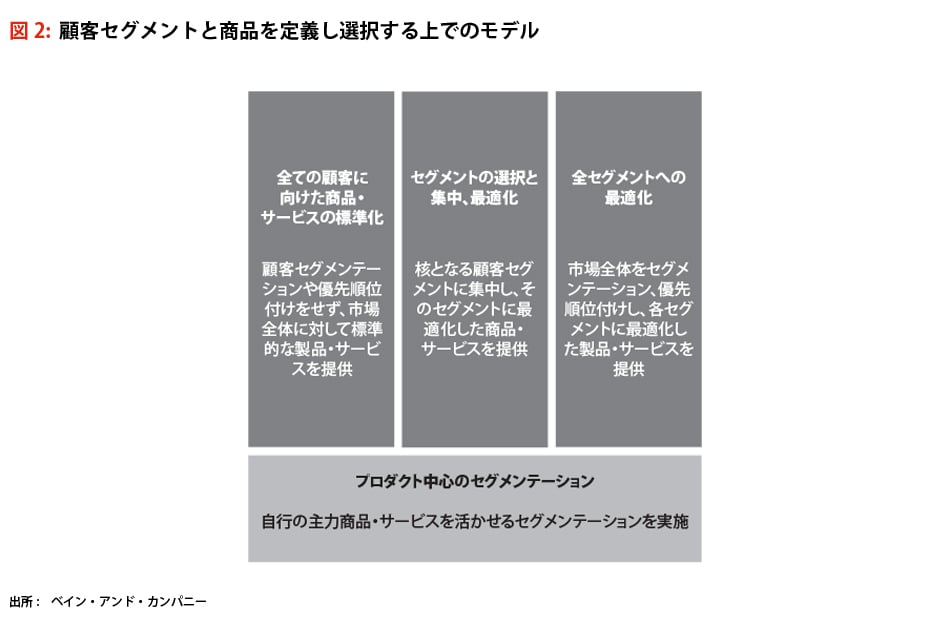

有効なセグメンテーションを行うためにはまず、特定の商品・サービスに特化してそれをあらゆる顧客に提供するのか、セグメントごとに最適化された戦略と訴求価値をもって、ターゲットとする顧客セグメントあるいは全顧客セグメントに対して事業を行うのかを決定する必要がある(図2)。

1つ目の選択肢は、特定の商品群を標準的な価格とシンプルなチャネルで全ての顧客セグメントに提供するというものであり、顧客の基本的なニーズにフォーカスする傾向のある地方銀行のほとんどは、このモデルを展開している。

2つ目の選択肢は、ターゲットとする顧客セグメントに最適化された商品・サービスを提供し、その他のセグメントに標準的な商品・サービスを提供するというものである。ドイツの多国籍銀行であるラボバンク(Rabobank)は、農業分野における専門性を用いて栽培中の穀物や家畜を担保とした融資や農具のリースなどの商品・サービスを提供し、米国の農業セグメントにおいてリーダーとなった。同様に、バンク・オブ・アメリカ(Bank of America)は医師に対する新規開業や機器購入のための融資、及びその際に必要な専門知識の提供を行っている。また同族会社をターゲットとしてサービスを展開しているシンガポールの銀行も存在する。

3つ目の選択肢の場合、銀行は全ての顧客をセグメンテーションし、それぞれに最適化された商品・サービスを提供する。JPモルガン・チェース(JPMorgan Chase)はこのモデルを採用し、12の業界において専門性を有している。

また銀行は特定の商品における強みを用いて差別化することで、商品中心のセグメンテーションを行うこともできる。例えばスタンダードチャータード銀行(Standard Chartered)や香港上海銀行(HSBC)は、中小企業向けの国際貿易金融に注力している。

いずれのモデルを選択しても利益を生み出すことが可能だが、一つのアプローチにコミットしないと中途半端な状態に陥ってしまう。例えば、組織とシステムを改変せずに特定の顧客セグメントに最適化したソリューションを提供しようとすると、事業が複雑化し利益を生み出せなくなる。一方で、十分な規模の顧客セグメントを得られないまま標準的なサービス提供に依拠すると、やはりポテンシャルを発揮することができない。

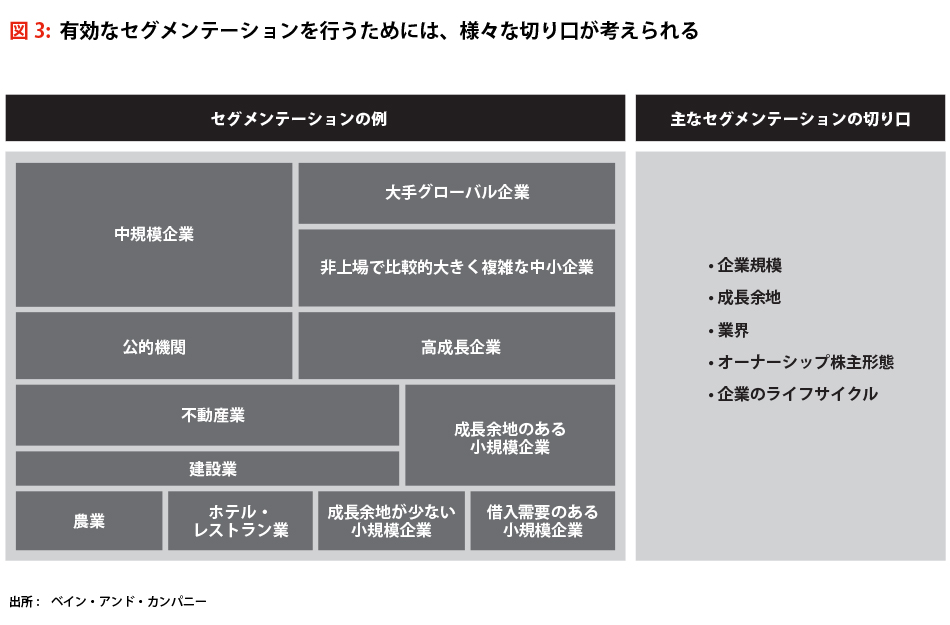

ターゲットとする特定の顧客セグメントを決定したら、次にそのセグメントの顧客の潜在的な支出額、成長性、ニーズ及び行動を詳細に理解する必要がある(図3)。

例えば、地域の小規模な小売店に訴求するためには、銀行としての基本的なニーズや、分散化されたキャッシュの取り扱いなどをおさえた、よく定義された分かりやすい商品・サービスを提供する必要がある。逆に、比較的大規模な不動産開発業者は総合的な融資とリスクソリューションについての専門的なアドバイスを求めており、起債やデリバティブ、資産運用などの商品・サービスに関する深い知見を重要視する。このように、顧客に関する包括的な理解と各セグメントで勝つための自行の能力に対する客観的な評価がそろって初めて、適切なセグメントの優先順位付けが可能となる。

セグメンテーションのスキームを選んだら、あるべき姿と目標する利益率、及び各セグメントで必要規模に到達できるような訴求価値を定義する必要がある。具体的には、それぞれのチャネルを通して提供する商品・サービス、各セグメントに対する融資の際の指針、市場進出と顧客獲得の方法を決定する。

訴求価値を形作るための選択は、どのような商品、流通方法、スキル、リソース、資本分散が必要か等、組織のあらゆる面に影響するだろう。銀行の制約とのギャップを明らかにすることは、投資に対するリターンを得るために重要だ。

どう勝つか

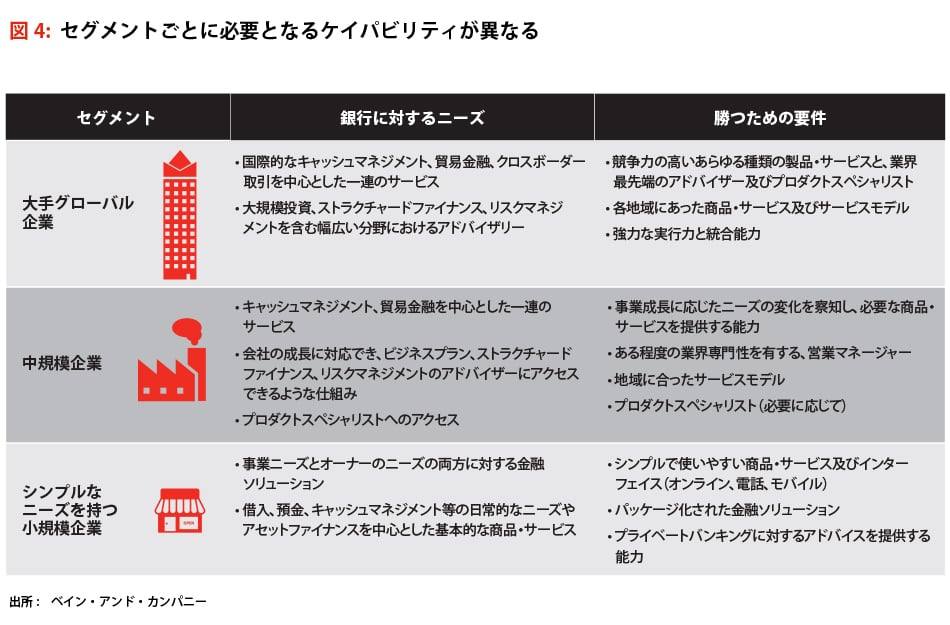

ビジョンと「どこで戦うか」を定義したら、「どう勝つか」を決断する。このプロセスでは、自行の置かれている現状だけではなく、自行の組織とケイパビリティの強み・弱みに関する明確な理解を必要とする。

どう勝つかを決めるためには、4つのエリア、すなわち商品・サービス、チャネル(既存チャネルとデジタル化したチャネルのバランスを含む)、全体プロセス、リスク管理を考慮する必要がある(図4)。

商品・サービス:巨大銀行の多くは、不必要に商品が複雑化して苦しんでいる。例えば、同じようなニーズとポテンシャルを持つ顧客が、異なる地域で、ひどい時は同じ地域の異なる支店から、バラバラに商品やアドバイスが提供されているケースもあろう。また、1つの商品であっても、価格や返済期間がわずかに異なるだけの数多くのバリエーションが存在する。このような複雑性によって、銀行が持続的に規模の経済によるメリットを享受したり、バックエンドのプロセスを高速化させたりすることは、もはや不可能となっている。

一部の業界リーダーは、商品の複雑性を管理し、営業のクロスセルを促進するために、顧客セグメントごとに異なるアプローチをとっている。ニーズがシンプルな小規模事業者には標準的な商品をパッケージ化して提供しており、例えば小売事業者向けのベーシックな「トランザクション&ペイメント」パッケージは、取引口座、オンライン及びモバイルからのアクセス、クレジットカード、クレジット決済サービスから成る。

一方で、比較的規模が大きく複雑な中小企業には、より洗練された付帯商品やアドバイザリーソリューションを提供する必要がある。これらのソリューションは、当該セグメントからの利益を最大限引き出すためには不可欠であるが、顧客担当マネージャーは往々にして、膨大な種類の商品を扱いきれず途方に暮れている。一部の銀行はこの状況に対応するために自行の統合ソリューションを明確に定義し、顧客担当マネージャーが理解できる数に絞り込んで提供している。例えば、複雑なニーズを持つ中小企業向けの「キャッシュマネジメント最適化」ソリューションは、融資と預金、e-ビジネスソリューション、貿易金融の標準的な商品に加えて、運転資本の最適化や流動性管理のアドバイザリーサービスを含んでいる。

銀行は自行が提供する商品を最適化するために、以下の決断を行う必要がある。

複雑性を最小にしつつ市場浸透率を最大にするために、どの中核商品とその付随商品をどの顧客セグメントに提供すべきか。例えばある欧州の総合銀行は、200以上の中小企業向けの商品について地域ごとの差をなくし、不必要な部分を積極的に減らした。そして、各顧客セグメントに顧客担当マネージャーがどの商品とパッケージを売るべきかを明確に定義することにより、小規模企業向けの約20の中核商品を明確に定義し、5つのベーシックなパッケージに絞り込んだ。その結果、顧客担当マネージャーは、はるかに明快に各商品を理解することが可能となり、クロスセルが促進され、顧客の取引完了までの期間を短縮することが可能となった

フルポテンシャルを達成するために、各商品をどのようにマーケティングするか。また、各モジュールやパッケージ、アドバイザリーソリューションのセールスコンセプトは、ターゲットとなる顧客セグメントにとって、どのようなものであるべきか

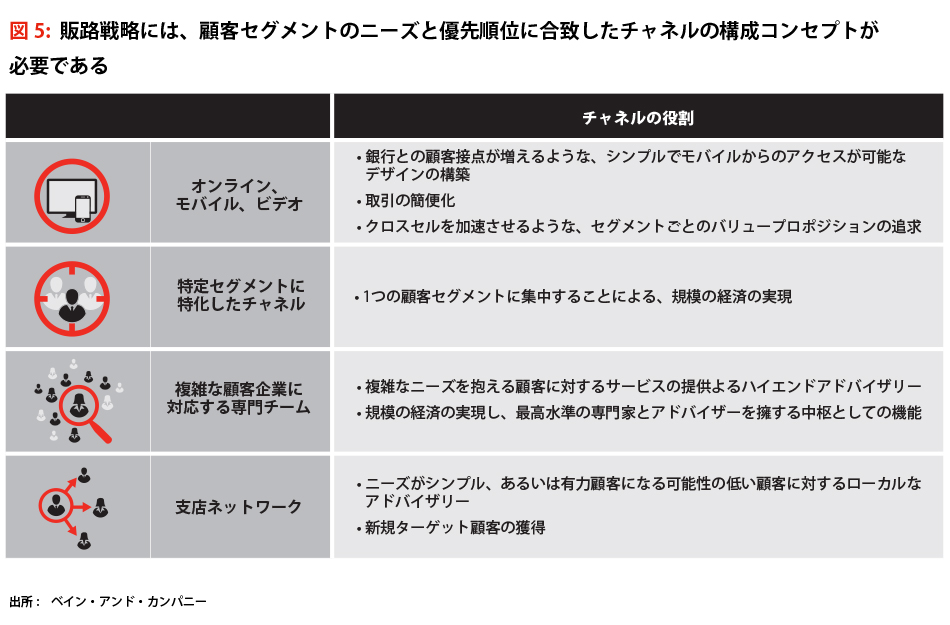

チャネル:デジタル技術によってチャネルは変貌してきている。それは主に、顧客が以前よりもオンラインとモバイルからのアクセスを期待していることと、フィンテック企業が金融業のバリューチェーンのいたるところに出現しているためである。銀行は顧客の認知形成から情報収集、購入、サービスの実施、体験の共有に至るまで、顧客との一つ一つの接点においてデジタル化されたチャネルと既存のチャネルとのバランスをどのようにとるのかを決定しなければならない(図5)。

小規模企業向け事業では、取引を既存の支店ネットワークからスケーラブルなオンラインとモバイルのプラットフォームに移行させデジタル化することにより、総コストが著しく低減される。さらにこの移行によって、標準的な商品・パッケージの提供が効率化される。また、中規模のより複雑な顧客に対しては、オンラインチャットとビデオ電話によって業界や商品の専門家へのアクセスを容易にすることで、デジタル化は競争のあり方自体を変える。

すでに自行の戦略上の意思決定に即した形で投資を始めた銀行も存在する。ある北欧の銀行は、比較的大規模で複雑な中小企業にフォーカスして事業展開することを決断した。それに伴い、商品に関する高度な専門家やシニア営業マネージャー、専門の融資戦略部隊と共に、集約されたハイタッチ金融センターへの投資を行った。このセンターは、既存のコールセンターと組み合わせる事によって、非常に小規模で単純なニーズを持つ顧客に対するコスト効率の良い直販チャネルとして機能させることもできた。

チャネルを適切に構成するため、銀行は以下の領域に関して決断する必要がある。

各顧客セグメントに対する、デジタルチャネルと既存のチャネルの役割は何か。顧客接点のうち、どれがデジタルで、どれが支店や営業所であるべきか(例えば、オーストラリアのウエストパック銀行(Westpac)は、柔軟なオンラインサービスと同時に、ビデオ会議のユーザビリティ向上に投資を行い、事業主がウエストパック銀行の専門家に遠隔地から直接アクセスできるようにした)

- 勝つためにはどのようなチャネル構成、ケイパビリティ、機能が必要か

- どのようにして優先順位の低いセグメントからの利益を最大化するか

最低限、どのくらいの数のチャネルの形態が必要か。どの顧客セグメントにどのチャネルを通して商品・サービスを提供するか

全体プロセス:過度に複雑なプロセスは単に銀行の利益を蝕むだけでなく、顧客の不満を生む。ほとんどの銀行ではプロセス全体の最適化はなされておらず、多くのプロセスで遅延や、貸出決定や顧客獲得といった重要な段階での情報不足に悩まされている。また、現場とサポート部門、オペレーション部門の間の責任範囲と意思決定権が明確に整理されておらず、無秩序な状態になっている。新しく導入されたものも含めて、中小企業向けバンキング事業の重要なプロセスでは、更新手続きを含め、与信プロセスが最も自動化されておらず、かつ細分化されており、それが重要なミス、手戻り、低い生産性の原因となっている。

銀行が、中小企業向け事業において顧客満足を向上させる統合的なプロセスを構築するためには、内部のオペレーション上の事情ではなく、顧客にとって重要な部分からプロセスを設計すべきである。デジタル技術は、それぞれの顧客接点における顧客体験を向上させる上でより重要になってきている。そして、一般的なITツールを全プロセスで用いることにより、自動化された、一貫したデータが確保される。

数々のフィンテック企業は、与信承認プロセスの大部分がデジタル領域で完結する環境を整備することによって、素早い融資決定とより良い顧客体験を実現している。例えば、ペイパル(PayPal)は中小企業向け融資事業に進出しており、銀行に対する代替サービスとして、自社の決済システム上の各店舗の取引履歴を用いた営業資金調達ソリューションを提供している。

フィンテックとの協業を選んだ銀行も存在する。OnDeckは融資を希望する小規模企業を審査し、わずか数分で貸出可否を判断する。米国最大の銀行であるJPモルガンチェースは彼らの成功に目をつけ、パートナーシップを組むことによって中小企業向け少額ローンのプロセスを劇的に高速化した。また、Regionsは近年、オンライン融資事業者のFundationと提携し、小規模事業者向けの貸付ソリューションを提供することを決断した。両社は、Regionsのブランドやリテールフランチャイズと、Fundationの迅速なオンライン融資承認プロセスとコンシェルジュサービスを統合することが相互の利益になると信じている。

リスク管理:信用危機は銀行のクレジット文化の欠点、事業上の優先順位と融資戦略との整合の失敗を露呈させた。多くの銀行は未だに鍵となる顧客セグメントの優先順位について深く考慮せずに、自行のリスク選好度と融資戦略を設定している。一般的に、融資戦略部隊と現場は接点がないため、信用供与とその更新プロセスがアカウントプランニング(顧客のサービス提案における戦略)と整合していない。

この状況は、以下のガイドラインに沿って融資及びリスク戦略を変革することで解決する。

- 「どこで戦うか」に応じた明確なクレジットポリシーの確立

- 資本効率とリスク回避の最適化を行うための、積極的なクレジットポートフォリオの管理

- 適正な能力を構築し、現場が融資の質に対して責任を持つ

- クレジットポリシーとプロセスのスリム化

これらのガイドラインは、年次のアカウントプランニングサイクルにおける融資プランニング、優先度の高いセグメントの顧客に対する意思決定プロセスの高速化、そして競争優位を実現させるための能力の基盤や専門的なチームの確立も意味する。

ドイツのウニクレディト銀行(ヒポフェライン)は、上記のガイドラインのいくつかの要素にフォーカスすることで効果的なリスクマネジメントシステムを作り上げた。彼らの取引ガイドラインには、資本効率に関する目標や、各取引が自行の対中小企業戦略に沿っているか等が含まれている。また、クライアントとアドバイザーのやりとりを明快にすることで査定プロセスを効率化し、顧客のパフォーマンスの厳格なモニタリングによって、関連する現場スタッフへの迅速なフィードバックシステムを構築することを可能とした。

変革を起こすための組織と現場のアクション

中小企業向けバンキング戦略を再考することは、多くの銀行にとって大規模な変革を意味する。変革は経営者がビジョンと戦略を設定するところから始まるが、競争に勝つ銀行は他の点においても以下のような行動をとる。

- 戦略、優先順位、新たに期待される行動が、現場まで周知されるようなコミュニケーション

- 特に顧客担当マネージャー、各商品の専門家及び融資戦略部隊の責任範囲の明確化と、それに対応するインセンティブの設定

各領域において最も競争力があり専門性を有する競合の特定と、チャネルのデジタル化やビッグデータ解析を含む、競合に勝つために必要となるあらゆるケイパビリティの獲得

市場進出のための各部門の協力。ある国際的な銀行では、国内の専門家チームに国内全ての商業不動産セグメントの顧客に対するサービス提供実施の権限を与え、他国チームとの経験の共有を推奨した。そのチームはすぐにクロスセルを加速させ、そこからの学びを他国のチームと共有した。また、同行は自行の最も優秀な融資担当者と複雑な中規模企業を担当する顧客担当マネージャーを特定し、融資戦略部隊と顧客担当部隊両方のニーズを満たすようなアカウンティングプラン用のテンプレートの作成など、カスタマーレビュープロセスを共同で再設計するように依頼した

多くの銀行にとって中小企業は未だに重要な顧客であり、どこで戦うか、どう勝つかについて適切かつ本質的な決断を行うことによって、持続的な利益を得ることができる。この市場で勝つためには、ターゲットとなる顧客セグメントと訴求価値を慎重に設定し、重要な部分に重点的に投資しつつ、競争優位性を築けない領域で戦うことを避けることが必要だと言えよう。