Etude

|

|

En Bref

In 2024, Bain & Company surveyed luxury leaders to understand their initial approach to AI. At the time, we found widespread interest and a desire to pioneer the technology—offset by reservations about its role in the customer journey. Despite broad enthusiasm, adoption was very low across most use cases. Written in collaboration withWritten in collaboration with

Since then, AI capabilities have accelerated dramatically, evolving from conversational tools and reasoning models into sophisticated autonomous intelligent agents. Consumers have embraced the technology, adopting large language models (LLMs) and generative tools at lightning speed. To capture this dynamic, we revisited our research. We found that rapid technological progress and employee adoption have accelerated executive agendas. Every luxury player now features AI on its strategic agenda. Nearly a quarter (22%) rank it among their top three priorities for the next three years, compared to only 5% in 2024, and 61% now place it within their top 10 (see Figure 1).

Figure 1

In total, 39% of luxury groups and Maisons now report having a defined vision, strategy, and sequenced roadmap for AI, while 48% noted having an AI vision with some pilots. Multi-brand groups are leading the way; all have defined a clear vision and roadmap for AI, befitting their role as central, vision- and standard-setting structures (see Figure 2). Maisons within these groups benefit from the corporate momentum, though their AI maturity varies by organization size and autonomy. Most independent Maisons, bar the largest ones, remain one step behind, constrained by limited internal resources and a reliance on external partners.

Figure 2

Note: Companies are considered “small” if they have less than €1 billion in revenue, “medium” if they have between €1 and €5 billion in revenue, and “large” if they have more than €5 billion in revenue Source: Executive Survey Comité Colbert x Bain 2026 (n=35 respondents; 23 Maisons/groups)Luxury AI deploymentsAdoption rates have increased across functions since 2024, signaling broader awareness and a growing appetite for AI. However, the industry largely remains in a state of experimentation. Growth has come primarily from pilots and tests rather than large-scale deployments (see Figure 3). The formula for successfully scaling and creating tangible business impact has yet to be defined.

Figure 3

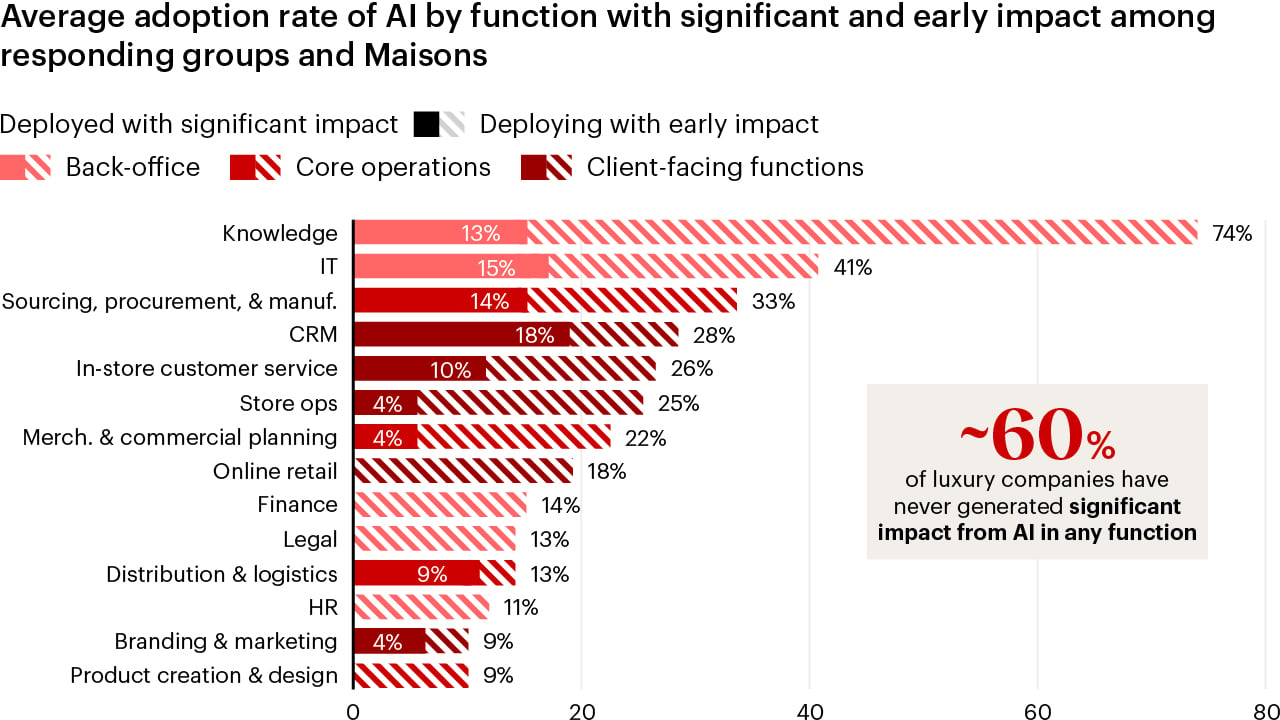

In luxury, AI is predominantly viewed as a lever for operational efficiency and productivity. This is consistent with views held two years ago, when the industry indicated a preference for AI to support “invisible” work and stay hidden from clients. Accordingly, support and operations functions have seen more progress in large-scale deployments compared to customer-facing functions. In back-office and core operations, knowledge management use cases have a 74% adoption rate, followed by IT (41%) and sourcing, procurement, and manufacturing (33%). On the customer-facing side, AI is still rarely deployed at scale, despite increased usage overall and a growing number of test cases. Online retail is among the least advanced areas in terms of large-scale deployment, even though it holds the greatest perceived potential benefit. Across functions, AI-driven impact remains the exception. Roughly 60% of luxury companies have yet to realize significant impact from any AI deployment. Even in areas where AI is more advanced—such as knowledge management, IT, and procurement functions—only 13% to 15% of respondents say these deployments have generated significant business impact (see Figure 4).

Figure 4

Consumers’ enthusiasm for AI is reshaping the luxury journeyDespite the industry’s decision to keep AI out of client-facing interactions, clients have welcomed it in. As of April 2026, 64% of Chinese buyers and 54% of US buyers said they used AI during their last luxury purchase, although that number was only 27% in France. The most valuable clients appear to be the most enthusiastic about AI. According to Bain research, 82% of very heavy spenders used AI for their most recent luxury purchase, compared to only 51% of moderate spenders and 28% of light spenders (see Figure 5).

Figure 5

This phenomenon crosses categories and channels. The share of clients who used AI for their most recent luxury purchase ranged from 55% to 58%, regardless of product category. Nearly half (47%) of in-store luxury buyers reported using AI during their shopping journey. This signals a new structural dynamic in luxury shopping—not a niche trend. Luxury shoppers who use AI reported using it mainly for discovery and comparison. About 64% said they used AI to research a product or brand, 60% sought styling advice or inspiration, 43% used it to summarize product reviews, 42% for price comparisons, and 41% to “complete a look.” Generalist AI tools are dominating early stages of luxury shopping for two reasons: their perceived neutrality and the current absence of brand-led alternatives. This behavior is expected to persist, driven by near-universal satisfaction. Roughly 97% of luxury AI users plan to use the technology again for an upcoming luxury purchase. Shoppers said the top advantages of using AI tools were faster and more objective decision making (cited by 68% of luxury AI users); reassurance on quality, fit, or product details (55%); and the discovery of products, options, and brands they would not have considered otherwise (52%). These perceived benefits imply both risks and opportunities for luxury companies. On one hand, they risk losing potential customers and narrative control—a dangerous drawback given the industry’s already-shrinking customer base. On the other hand, AI presents major opportunities to build relevant brand awareness, reinvent acquisition, reinforce brand messaging, enrich the sales process, and elevate client experiences. Generative search visibility is the most pressing battlegroundGenerative engine optimization (GEO) is reshaping discoverability: how brands are surfaced, cited, and described in AI-generated search answers. Most organizations are only beginning to address this change. Currently, only 48% of groups and Maisons regularly track their AI search and GEO performance. Only 10% consider themselves strong on generative visibility, while more report their performance as moderate (52%) or weak (29%). In partnership with Meikai, we analyzed consumer search behavior on generative engines, uncovering new insights about how to win visibility:

How to appeal to LLMs: Emerging GEO best practicesTo rank well in generative engine results, luxury companies must:

These principles cannot be implemented effectively as isolated, one-off actions. Effective GEO will require cross-functional coordination across teams that learn and adapt together, such as search engine optimization, public relations and media, marketing and communications, technology, data, customer relationship management (CRM), and customer experience. In owned channels and touchpoints, AI has upside potential—but the industry is proceeding with cautionAI has the potential to reshape every stage of the customer journey, from discovery to loyalty. When it comes to customer-facing AI, however, the industry is largely stalled in a state of reflection and testing (see Figure 6). Leaders are highly aware of AI’s potential to support client interactions but remain cautious of transformative deployments, fearful of betraying luxury codes.

Figure 6

Beyond GEO, four AI innovations have the potential to transform client interactions. We measured the industry’s progress on them specifically:

The gap between ambition and execution is often deliberateMost leaders agree on the massive potential of AI, but the frenetic pace of innovation cycles has triggered two contrasting responses. Some executives have adopted a protective posture, stepping back to pause and evaluate. Other are overwhelmed by an urgency to adapt their organizations and governance models. For the former, the gap between AI ambition and execution is not a sign of lagging but of a deliberately selective and cautious stance. Operating with a high-stakes customer base leaves little room for error, and executives are wary of disappointing clients or deploying solutions that could become obsolete within months given the speed of innovation. These leaders are also taking great care to protect the codes of luxury. Rather than rushing to market, they are taking time to define what an AI-augmented customer experience should look like, committed to preserving the deeply human touch that defines luxury. For some, that means keeping AI entirely out of customers’ direct contact. To generate impact at scale, luxury must move from tests to structured transformations around key business domainsSeeing this moment clearly—and scaling successfully—requires intense focus. To generate meaningful results, the industry must pivot from running multiple concurrent yet isolated test cases toward a structured transformation. Scalable initiatives should be structured around use cases that completely transform end-to-end processes, rather than incremental improvements to an individual’s productivity or quality. Use cases can be built around roles (such as sales advisers or marketing managers) or processes (such as content creation or product development), but they only become transformational by targeting areas of meaningful value in the organization. Executive teams should initiate and drive this transformation, as they are uniquely positioned to define what is “transformational.” They have the clearest insight into where opportunities, investments, and costs are concentrated, and they can identify and prioritize core business activities for AI to address. Without such influence, AI initiatives risk being adopted by isolated functions or teams, resulting in lower impact. Executive commitment is a recognized prerequisite for success. Nearly 70% of luxury executives cited “sponsorship from leadership” as the most critical enabler for AI development. Conversely, the most commonly cited barriers to AI adoption were difficulty defining a clear, value-oriented strategy (60%), lack of internal resources (60%), and lack of executive support (40%). Next steps for luxury companiesWith leadership commitment in place, companies must manage the balancing act between progressing AI and retaining control. A number of measures can help them walk the line: Establish AI governance and prioritiesA governance charter should describe how the organization intends to deploy AI across the organization and the customer journey. From there, it becomes easier to prioritize a limited number of work streams where AI can support end-to-end process redesign or completely transform a key scope of work. Companies also need governance guardrails that are specific to AI. A wider stakeholder perimeter—encompassing technology, operations, and change management—is required to actively mitigate emerging risks. Organizational programs covering process, culture, and training can help support uptake and maturity. Strengthen data foundationsData must be treated as a strategic corporate asset, especially data linked to AI priorities. As one luxury Maison said: “No tech, no data, no AI.” Some organizations may need to strengthen their technology foundations to enable structured data collection. Deploy and measureTo generate meaningful gains and fund future investments, leaders should deploy and scale the most mature operational use cases—and thoughtfully measure the results. Assess the return on investment of AI agents carefully, continuously rethinking how technology costs are analyzed and allocated. For example, a declining cost per token could be offset by model upgrade costs or by rising token consumption, which may be driven by multistep agentic reasoning. The investment logic should include cost breakdowns by function and team rather than just a centralized overview. Monitor technological progress and create dynamic roadmapsWhile luxury is accustomed to long horizons and multiyear cycles, this new fast-paced reality calls for short and revisable roadmaps. Companies can establish observatories to monitor the AI ecosystem and adopt a more dynamic stance. Luxury leaders must also observe consumer behaviors, both in luxury and the mass market. Evaluating choices made by market leaders and best-in-class players from other sectors can help inform future decisions. ConclusionThe luxury industry is wary of AI; its clients are not. In just two years, consumer behavior has radically changed, with shoppers embracing generative tools and remapping the entire luxury journey. LLMs are the new digital concierge, pointing shoppers toward brands and subtly shaping purchase decisions. To keep pace with this structural change, luxury leaders must answer two urgent questions: Can LLM agents find your brand? And how could AI meaningfully enhance client experiences and relationships? Answering these questions requires mastering the fine art of balance across three tensions:

Critically, “augment” and “enhance” do not mean “hand over.” Luxury companies can preserve high-touch services and human-to-human interactions without relinquishing control to bots. Technology can continue working behind the scenes in support of client relationships, orienting sales advisers toward the best customers to contact, at the most opportune times, and with the most resonant messages and offers. Clients now expect exceptional service and augmented experiences. Luxury companies must determine exactly where they can leverage AI to create the most value across the shopping journey. Exceeding client expectations remains a foundational code of the luxury industry—but it requires a new set of tools. Comité Colbert and Bain & Company would like to extend their sincere gratitude to all the individuals and Maisons (members of Comité Colbert and beyond) that contributed to this study, responding to the survey and sharing their perspectives on artificial intelligence during interviews. In particular, we thank the following Maisons and groups for their valuable participation: Balenciaga, Biologique Recherche, Boucheron, Carita, Cartier, Celine, Chanel (Fashion division), Christian Dior Parfums, Christian Louboutin, Diptyque, Givenchy, Hermès, Kering, Longchamp, L’Oréal Luxe, Lorenz Bäumer, Louis Vuitton, LVMH, Messika, Richemont, Van Cleef & Arpels, and Yves Saint Laurent Beauté. About Comité ColbertFounded in 1954 by Jean-Jacques Guerlain, Comité Colbert is a unique collective gathering 98 French luxury Maisons, 17 cultural institutions, and six European luxury Maisons. Through its members, Comité Colbert unites 14 different métiers: crystal, leather goods, design, publishing, faïence and porcelain, gastronomy, haute couture and fashion, jewelry and horology, music, silver smithery, luxury hotels, fragrance and cosmetics, heritage and museums, and wines and spirits. Comité Colbert’s mission is conveyed in its raison d’être: to passionately promote, to sustainably develop, and to patiently transmit French savoir faire and creation to infuse a new sense of wonder. Our actions aim to collectively promote French art de vivre on the world stage, to preserve French savoir faire and creation, and to participate in their transmission to new generations. |