Report

|

|

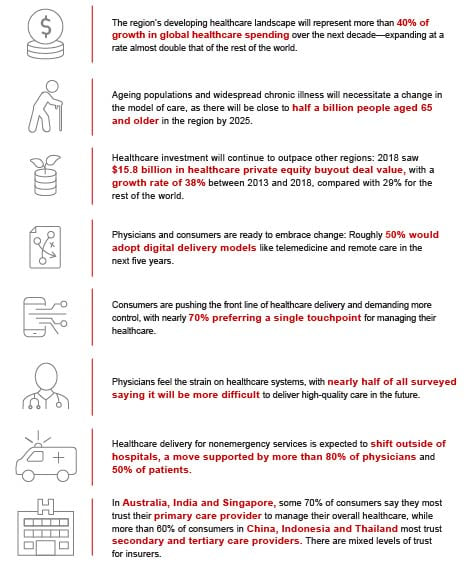

Healthcare players in the Asia-Pacific region are in for a wild ride. Explosive growth combined with changing demographics and shifting consumer expectations will inevitably lead to significant transformation. By 2025, close to half a billion people across the region will be aged 65 or older. Not only is the population as a whole ageing, it is also getting sicker. As the demand for chronic care management outpaces that for acute care services, expenditures will grow at double the rate of the rest of the world. Consumers and physicians alike are starting to feel the squeeze. Consumers are increasingly frustrated by long wait times and high costs. They want more convenience, more emphasis on wellness and preventative services, and more control over their healthcare. Meanwhile, physicians feel ill-equipped to deliver high-quality care given all the changes taking place. To better understand the region’s challenges and opportunities, Bain & Company surveyed more than 1,800 consumers in Australia, China, India, Indonesia, Singapore and Thailand, and more than 250 physicians in Australia, China, India and Indonesia. The results shine a spotlight on a region primed to reshape its healthcare landscape. Our survey found that healthcare systems across the region need to undergo transformational change—and that the timing couldn’t be better. Consumers and physicians alike recognise that the status quo is unsustainable. At the same time, the region is the fastest-growing destination for healthcare investment globally. These dollars are fuelling growth as well as improving the quality of care. Moreover, the emerging nature of many Asia-Pacific markets makes them more adaptable to change, and several governments are already evaluating and launching reform efforts. To be sure, the challenges facing the region are manifold. But the conditions are favourable for stakeholders to not just manage but also lead the changes ahead. We believe that Asia-Pacific countries can improve the quality of care and hold the line on skyrocketing costs while doing a better job satisfying consumer and physician expectations. To achieve this, stakeholders must empower consumers to manage their care, transition nonemergency care out of hospitals, increase consumer access to digital tools and platforms, and support physicians with new technologies. Of course, specific strategies will vary by country. But stakeholders that seize the moment could reshape healthcare in a way that serves as a model for countries around the globe. Six factors that are influencing changeAsia-Pacific stakeholders have an unprecedented opportunity to transform the region’s healthcare landscape. To create a framework for transformational change that sticks, stakeholders need to have a clear-eyed understanding of the forces at work in their respective markets. Our 2019 survey uncovered six factors that are altering healthcare across the region in deep and lasting ways. These trends are by no means unique to Asia-Pacific. But the scale at which they are occurring is unparalleled compared with the rest of the world. Factor No. 1: Changing demographics. Populations across the region are getting older and sicker. By 2025, 460 million individuals will be over 65 years of age. This population will make up approximately 60% of global growth in this age group, compared with approximately 22% from EMEA and 18% from the Americas. At the same time, an estimated 265 million people will be diagnosed with diabetes, and 250 million over the age of 18 are expected to be obese. All these factors will necessitate a shift from acute care services to chronic care management. Factor No. 2: Rising costs. Costs are rising faster than real wages, with spikes in Australia and Singapore at 3.3 times and 7.8 times, respectively. Across the board, 57% of consumers find out-of-pocket medical bills to be unaffordable, and 42% find private insurance premiums to be out of control. Their concerns are shared by physicians across all countries. Factor No. 3: Shifting consumer expectations. Consumers are frustrated with the current state of healthcare. Their top four sources of frustration involve wait times and healthcare costs (see Figure 1). At the same time, a new type of consumer is emerging, one who is more interested in overall wellness and more informed about conditions and treatment options than before (see Figure 2). Consumers’ changing expectations will only intensify their dissatisfaction with their local healthcare systems.

Figure 1

Figure 2

Factor No. 4: Technological and medical transformation. Asia-Pacific consumers are fully embracing the digital era, with greater connectivity and digital penetration evident across the region. For example, mobile wallet penetration is 65% in China and 60% in India, compared with 16% in the US and 12% in the UK. And while rates of digital uptake vary by country, data and analytics are already changing the way healthcare is delivered across the region. Technological advances also promise to disrupt medicine as we know it. Personalised medicine could make the traditional notion of “one size fits all” healthcare obsolete, and resources are increasingly being deployed towards research. Factor No. 5: Physician capacity. Against this backdrop, physicians feel they can’t keep pace. Fully 87% of respondents believe they need to be aware of a broader range of treatment protocols than five years ago, and 66% find it challenging to keep current on new treatment options (see Figure 3). More alarming, nearly half believe it will be more difficult to deliver high-quality care over the next five years, due to factors such as shortfalls in funding and resources, rising costs, changing patient expectations, perceptions of trust and the cost barriers to adopting new technology (see Figure 4).

Figure 3

Figure 4

Factor No. 6: Regulatory environments. Regulators are increasingly playing an active role in addressing access, cost and quality constraints. This trend is evidenced by moves towards universal healthcare in markets such as China, Indonesia and, more recently, India and the Philippines. Many regulators are also recognising that digital solutions will be critical to care delivery, which is shaping policy reform and creating opportunities for greater coordination. The potential for a crisis in healthcare quality, accessibility and affordability looms large. However, this worst-case scenario is not assured. Rather, the region is at a crossroads, where some of the most promising trends can be used to reimagine care delivery in a way that puts consumers at the centre. A new framework for healthcare deliveryWhere stakeholders land in this rapidly changing landscape will depend on their ability to meet the changing needs of consumers and physicians. While each country’s specific situation will dictate the best path forward, our research revealed four universal opportunities that stakeholders can pursue as they look to reinvent their healthcare systems. Opportunity No. 1: Empower consumers by providing a single touchpoint for care. Consumers increasingly want greater ownership of their care, but the often-siloed nature of healthcare systems makes this difficult. It’s unsurprising, then, that nearly 70% of respondents expressed the desire for a single touchpoint, either physical or virtual, for managing their healthcare (see Figure 5). Healthcare players can empower consumers to take charge of their care by providing a single, trusted resource through which to navigate their options.

Figure 5

Opportunity No. 2: Transition care outside of hospital walls. Shifting nonemergency services from hospitals to outpatient settings or alternative delivery models will be key to relieving the burden on overextended hospitals. Roughly half of consumers surveyed would be comfortable receiving services in an outpatient setting, and more than 80% of physicians believe a number of nonemergency services could be offered outside of hospitals (see Figure 6). Moreover, physicians are open to shifting some services to digital or virtual platforms, or to relying on assistance from nonphysicians through the use of artificial intelligence (AI) or machine learning (see Figure 7).

Figure 6

Figure 7

This shift in delivery will only be successful if consumers and physicians believe the quality of care is equal to or better than that delivered in a hospital. Stakeholders will need to tread carefully here, weighing the potential for cost savings and improved access against deeply entrenched perceptions within the populations they serve. Opportunity No. 3: Increase consumer access to digital tools and platforms. In response to consumers’ desire for anytime, anywhere access to healthcare, stakeholders will need to invest in world-class digital tools and online platforms, including telemedicine. Our survey found that the use of self-diagnosis apps, long-term illness management tools and electronic records is likely to increase significantly over the next five years (see Figure 8). Notably, 46% of consumer respondents expect to use telemedicine in the next five years—an increase of 109% over those who use it today.

Figure 8

Despite the high levels of support for telemedicine, many consumers prefer face-to-face care. With that in mind, stakeholders will need to develop digital and bricks-and-mortar hybrids that integrate online and offline models. Opportunity No. 4: Support physicians with new technologies. Physicians are cognisant of the growing chasm between consumer needs and their ability to deliver. They fully expect to increase their use of AI and machine learning in the next five years to bridge the gap (see Figure 9). Better clinical decision-making resources and tools are one area where respondents indicated the need for support. Investing in new technologies and AI could be key to shoring up physicians’ capacity for managing chronic diseases and providing preventative care.

Figure 9

Building trust is keyConsumers and physicians want more from healthcare players: more innovation, more collaboration, and more solutions for lowering costs and solving complex healthcare challenges. Our research found that consumers have very clear expectations for primary care providers, hospitals and health insurers (see Figure 10). The shift towards personalised preventative care and wellness, along with concerns about access to care and rising costs, is readily apparent in what consumers want from these stakeholders.

Figure 10

Physicians, too, want to see more from healthcare players (see Figure 11). Tellingly, physicians across specialties believe that primary care providers should be the single point of contact for coordinating care. With the exception of respondents from Australia, physicians also by and large believe that insurers should take an active role in care provision.

Figure 11

Transformation at this scale cannot happen without activating the right players in the right way to deliver on consumer and physician expectations. Understanding and responding to consumers’ levels of trust in each player will be critical (see Figure 12). Levels of consumer trust vary by country, underscoring that there is no broad-brush solution to the region’s healthcare challenges.

Figure 12

Adapting to a new realityWhile our survey revealed universal opportunities for transforming healthcare in the Asia-Pacific region, not all paths lead to the same destination. Every country must develop strategies to address its unique challenges and constraints (see Figure 13). Each country is also starting at a different place in terms of consumer and physician satisfaction—which could make change more challenging for some than others (see Figure 14). Our recommendations for each country take these factors into account to define a path that best supports sustainable transformation.

Figure 13

Figure 14

AustraliaAustralia’s world-class healthcare system is at a crossroads. Significant healthcare cost inflation, a private healthcare system facing a “death spiral” and a public healthcare system feeling the strain of declining government funding and growing patient volumes are leading to an impending crisis that can only be addressed with fundamental reform. Both private-sector players and federal and state governments must act to achieve the urgent structural change that is required:

ChinaThe healthcare landscape in China is challenged by costs and access to care. Consumers and physicians are well aware of the uneven distribution of resources across different tiers of cities. However, trust has surfaced as a third and significant challenge. Consumer trust in emerging private-sector providers still meaningfully lags trust in public hospitals, and Chinese consumers increasingly trust digital health platforms over physicians. As a result, healthcare players must address the following four areas:

IndiaAffordability, access and quality are all pressing needs for India’s healthcare system. The government is attempting to address affordability by extending coverage to 500 million beneficiaries through the Ayushman Bharat national health protection scheme. Improved access, however, faces major bottlenecks at both the infrastructure and the physician levels. Strong government regulatory action to control pricing is also prompting concerns about quality and cost/viability issues amongst physicians. Based on our survey findings, the following three factors are key imperatives as forces of change:

IndonesiaIndonesia’s hospital-centric market is struggling to meet both consumer and physician expectations for care. In addition to concerns about high costs and poor quality, respondents indicated that a lack of adequate insurance, insufficient healthcare talent and the absence of high-tech facilities are challenging the system. Change will need to happen rapidly. The 2011 launch of BPJS Kesehatan has transformed affordability, but it has also unleashed a wave of demand on an already straining system. In light of these challenges, healthcare players should prioritise the following three areas to scale up service delivery and quality of care:

SingaporeOne of the world’s most advanced healthcare markets, Singapore delivers measurably better outcomes at a fraction of the cost of the US. The country’s thriving outpatient ecosystem is triaging care away from hospitals and driving preventative behaviours. However, healthcare costs are still escalating at a blistering rate of 10% annually, provoking a multipronged government response. We believe the country’s best approach is to concentrate on these three priorities:

ThailandIn Thailand, our survey uncovered a significant disparity in consumer satisfaction between primary and secondary care clinics. Despite consumer preference for secondary care centres, Thailand’s urban areas have a broad network of primary care clinics. Upcountry, district hospitals that serve as a point of primary care and local health centres have negative Net Promoter Scores, a metric Bain uses to measure customer loyalty and satisfaction. Thailand is the only country we surveyed where consumers rated access to care, availability of medical resources and quality of care as their top concerns—a legacy of the 30-baht healthcare scheme initiated in 2001. To encourage transformation in this market, healthcare players should:

Implications for the futureAsia-Pacific’s healthcare landscape will look very different five years from now. Regional stakeholders have the power to determine whether the changes are the result of unchecked market forces or of a methodical reframing of the front line. Opportunities abound for players that can win the trust of consumers and embrace data and the digital wave. But to stake a lasting claim in this new landscape, healthcare players will need to adjust rapidly to regulatory changes, advances in technology and medical developments. Stakeholders must also be ready to embrace new arrangements with traditional competitors to reframe care models and create a seamless patient experience. The market will not wait for incremental change. The front line is demanding bold, structural transformation now. Healthcare stakeholders with strategies that are responsive to consumers and physicians will quickly emerge as the front-runners in this dynamic environment. Lucy d’Arville is a partner with Bain & Company’s Healthcare practice in Australia. Satyam Mehra is a partner in Bain’s Healthcare practice and is located in New Delhi. Alex Boulton is a principal in Bain’s Private Equity and Healthcare practices and is based in Singapore. Vikram Kapur is a partner and leads Bain’s Healthcare practice in Asia-Pacific from Singapore. |