Brief

|

|

In evidenza

Over the past decade, sovereign wealth funds (SWFs) have become pillars of global capital markets. Fueled by strong portfolio returns and steady state capital injections, SWFs have expanded faster than any other institutional investors. That trajectory is expected to continue, with SWFs projected to reach $30 trillion in assets under management (AUM) by 2035. However, the roadmap for growth is changing. The conditions that enabled historical growth are shifting, unsettled by higher interest rates and increasing volatility in hydrocarbon revenues. The effects of geopolitical fragmentation, technological disruption, and the energy transition are also intensifying—and redefining where and how sovereign capital can create value. For the first time, Bain & Company surveyed leaders from eight SWFs to understand their priorities and how they are operating under pressure. While industry terminology varies, in our research, “SWFs” describe investors and investment vehicles owned by sovereign entities or nations. Our sample represented half of addressable SWF AUM. The responses reveal several trends, plus four imperatives for navigating this new environment. It’s impossible to discuss SWFs without acknowledging the regional and broader conflicts affecting the Middle East. While responses in this report reflect conditions at the time (late 2025 and early 2026), they are not shortsighted. Investing is inherently a long game. As of this writing, we have no evidence that the long-term priorities of SWFs have changed. If anything, current events have sharpened their focus on supply chain resilience and security, the diversification of strategic partnerships (notably with Asia), and the monitoring of local economic impacts, including fluctuations in oil and gas revenues. If these conflicts are resolved relatively soon, countries may not need to draw on these funds to cover the financial costs of war. However, this is an evolving situation that we—and the world—will continue to watch with hope and compassion. The continued rise of SWFsIn recent years, SWFs have expanded substantially, both in real terms and in their influence and sophistication. SWFs reached $15 trillion in AUM in 2025, reflecting a 10.3% CAGR—and outpacing every other class of institutional investor (see Figure 1).

Figure 1

The top 10 funds hold more than 75% of total wealth, concentrated in the Middle East (40%), Asia (40%), and Europe (20%). SWF growth was powered by two main sources: 75% came from traditional financial performance and portfolio returns, while the balance came from state capital injections. Notably, this growth profile differs for funds that receive regular government support. For those entities, portfolio returns and state injections contributed equally (50/50) to their expansion. State injections included approximately $890 billion in budget surpluses, mostly from hydrocarbon revenues. State asset transfers were also significant ($480 billion) and included the transfer of Saudi Aramco shares into the Public Investment Fund (PIF) and state-owned enterprise (SOE) transfers into Abu Dhabi Developmental Holding Company (ADQ)—assets which were recently transferred to L’Imade, a newly established investment entity. Indonesia also injected capital by launching the Danantara Indonesia superfund with an initial $170 billion in state assets. Across the board, dividend distribution and borrowing have remained relatively limited, allowing SWFs to reinvest gains and amass wealth at an accelerated pace. And that trajectory isn’t slowing. AUM is expected to reach $30 trillion by 2035, continuing to grow at an 8%–9% CAGR. But the roadmap is likely to look different based on a fund’s archetype. Defining characteristics of SWFsSWFs are defined by unique combinations of mandate, asset allocation, and capital deployment. Return-focused vs. dual-mandate fundsAll SWFs are expected to meet return thresholds. Based on our research, more than 60% of SWFs target annual returns exceeding 6%–8% over the next five years. However, each fund also has a specific raison d’être—a purpose that falls somewhere between purely financial motivations and national objectives.

About half of the top 20 SWFs have a stated commitment to their local economies, yet only a third of global SWF AUM is allocated to local assets or development agendas. Many of the largest funds face limits on investing at home. Asset allocation and capital deploymentWhile portfolios remain anchored in public markets, they are shifting toward private assets. Across the top 20 funds, approximately 70% of AUM sits in public markets and 30% in private markets (e.g., private equity [PE], infrastructure, real estate, venture capital, and private credit). There are notable variations, though: In Europe, NBIM is fully public, and the Kuwait Investment Authority remains mostly public. Public holdings are largely passive or minority stakes; only 20%–25% of SWFs hold strategic or controlling positions. The portion of AUM allocated to private markets is becoming more active, and funds are increasingly likely to manage these exposures in-house rather than through third-party managers. Direct or coinvestments account for 50%–60% of investments, outpacing indirect general partner (GP) commitments (see Figure 2). PE is the largest private allocation (50%), followed by infrastructure and real estate (both at 25%).

Figure 2

A shifting landscape for SWFsBuoyant markets have flattened. Hydrocarbon revenue, which has been the largest source of budget surpluses, is now uncertain. Asset transfers are slowing now that the bulk of SOE transfers are complete. In short: SWFs are operating in a different world. In this environment, higher interest rates are driving the cost of capital and compressing valuation multiples. Volatile hydrocarbon pricing makes cash flow less predictable. And private markets—previously the main engine of outperformance—are maturing. Liquidity remains uneven, and value creation increasingly requires active ownership and operational excellence rather than passive exposure. And that’s not all. Beyond these financial dynamics, structural forces are redefining sovereign investing. Geopolitical fragmentation is reshaping investment corridors, while rapid technological disruption is changing both what SWFs invest in and how they operate. Meanwhile, the accelerating energy transition is redirecting capital toward renewables, decarbonization, and sustainable infrastructure. Four growth imperativesWe asked SWF leaders how they plan to sustain growth in the decade ahead. They cited four priorities (see Figure 3):

Figure 3

Recalibrating capital deploymentLeading SWFs are rebalancing their portfolios to reflect new macroeconomic and geopolitical realities and enable greater flexibility. They’re also becoming more active in deployment across investment themes, regions, and asset classes. Based on our research, capital deployment is shifting in four distinct ways: Trend 1: Alternatives have gained staying powerThe most notable shift in capital deployment over the past decade has been the steady increase in alternatives. They now account for approximately 30% of AUM, up from around 20% in 2015. In our research, SWFs consistently ranked alternatives as their top capital deployment priority for the next two to three years (see Figure 4).

Figure 4

Among alternatives:

Trend 2: Direct access models are growingOver the past decade, the era of passive limited partnership commitments with larger PE funds has given way to a more active, partnership-driven approach. More than 80% of the SWFs we surveyed expressed a desire to increase their coinvestment allocation. This shift is consistent with broader direct and coinvestment trends. Coinvestments and direct investments now represent 50%–60% of SWF private deployments—up from approximately 40% in 2023. In the past 12 months, sovereign investors participated in approximately $160–$170 billion in global private market transactions, of which $120 billion was through direct investments. According to Global SWF, direct investment totals have averaged $120–$130 billion over the past five years. In addition, SWFs are starting to dominate large mergers and acquisitions (M&A) deals, leveraging their capital scale and reach. Examples are abundant:

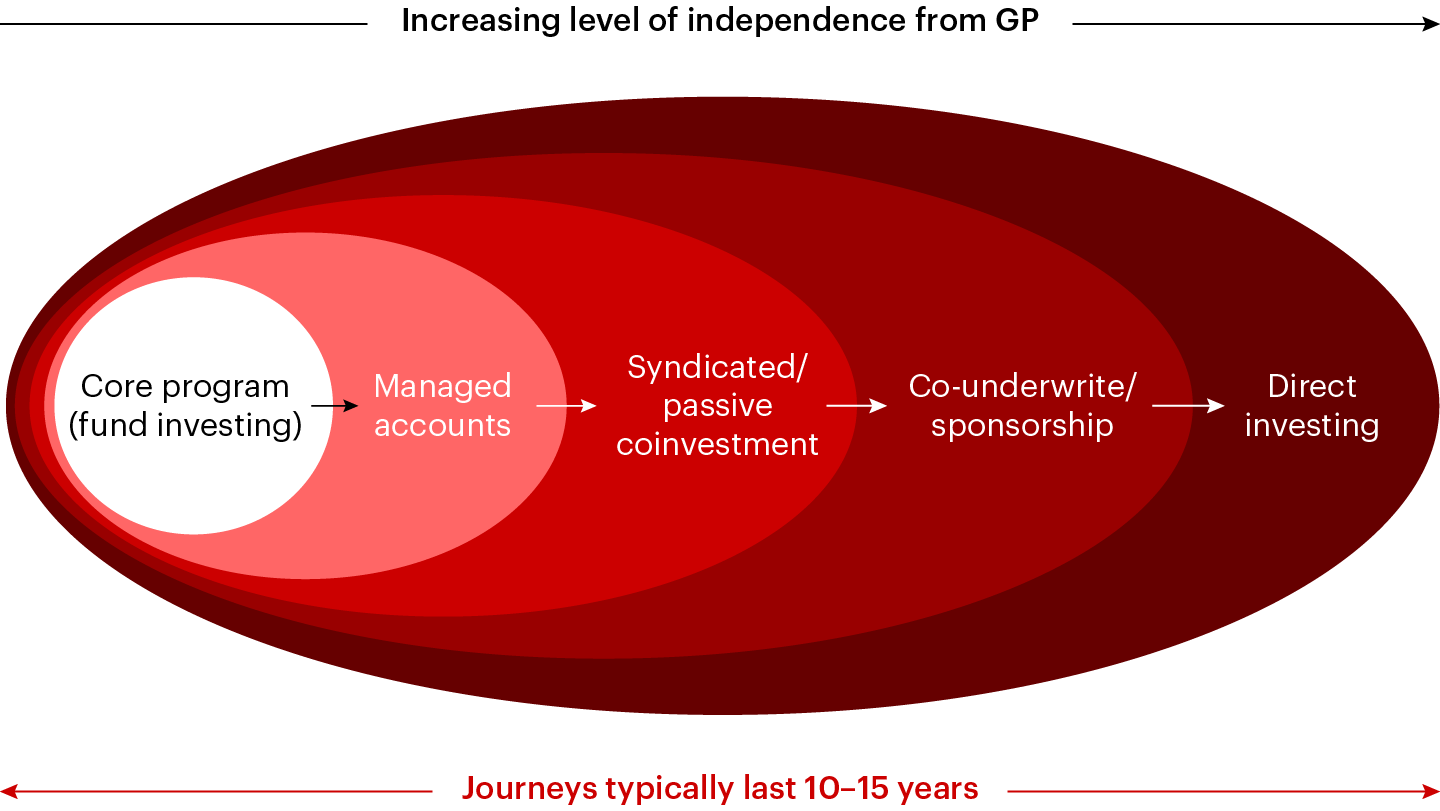

SWFs have been transitioning from indirect to direct investing over the past 10–15 years, lessening their reliance on GPs as they develop their own portfolio management and value-creation capabilities (see Figure 5).

Figure 5

At the start of the transition, SWFs leveraged limited partnerships to invest in funds managed by others (e.g., funds of funds or separately managed accounts). As they sought more control, funds engaged GPs to manage customized investments and increase exposure to specific themes. Over time, PE firms began offering coinvestment rights on larger deals—shifting the relationship from “fund manager and client” to “equal strategic partner.” To play this more active role, SWFs had to build internal capabilities in due diligence, investment decision-making, and financing. Today, many funds possess the deployment scale, talent, and governance structure needed to coinvest alongside GPs or lead direct investments independently. Direct access gives SWFs tighter control over capital deployment, reduces fee leakage, and allows funds to retain a larger share of the value they help create. Trend 3: Geographic interests are shifting eastMore than 80% of the SWF leaders we surveyed expect to increase their allocations to Asia (excluding China), while half plan to expand their exposure in Europe. This geographic reweighting gives SWFs an opportunity to diversify—aligning with the world’s fastest-growing economies while hedging against Western valuation peaks and political scrutiny. Beyond diversification, Asia offers a deep pool of potential strategic partners and access to high-growth opportunities. As Asian economies expand rapidly, local companies are seeking global capital and expertise to help them scale internationally. This creates a natural hub for coinvestment and long-term value creation. Mubadala announced plans to double its Asian exposure by 2030, increasing the region’s share of AUM from 12% to 25%. Trend 4: New funding sources are fueling expansionThe top 10 SWFs hold investment-grade credit ratings—and they’re leveraging these strong scores to open new sources of funding and liquidity. Among top funds, structured leverage and debt-to-AUM ratios have risen steadily, increasing from 0%–5% in 2019 to 10%–15% in 2025. PIF led this shift, becoming the first SWF to issue a green bond in 2022 ($3 billion). Additional bonds and sukuk (Islamic bonds) followed—totaling more than $30 billion by 2025—with each bond heavily oversubscribed. Mubadala took a similar path in 2025, broadening its funding base with $750 million in 10-year bonds and launching dirham-denominated notes. Beyond debt, SWFs are also monetizing and recycling capital from mature assets to fund new opportunities. Mubadala monetized its position in GlobalFoundries through an initial public offering in 2021 and a secondary sale in 2024, redeploying the proceeds into high-growth technology and infrastructure investments. PIF has also recycled capital, selling 120 million shares of Saudi Telecom Company in 2021 and an additional 100 million shares in 2024 while remaining the company’s majority shareholder. Similarly, GIC is divesting $1 billion in PE fund interests across roughly 30 secondary market funds to reinvest in higher-growth channels. Delivering on their dual mandate and value creationBalancing financial performance with national economic development is a central theme for most SWFs, though it manifests in different forms. Some funds focus on supply chain security and control to secure national resilience. For example, they gain strategic access to critical raw materials, manufacturing processes, or food supply. Others are dedicated to local GDP growth and job creation. These funds pursue diversification by accelerating existing sectors or seeding entirely new ones to drive local growth. Translating these national ambitions into measurable economic outcomes is often a multi-decade journey. Currently, 11 of the top 20 SWFs explicitly pursue dual mandates. Those that succeed share six foundations:

Unlocking value from AIAI is both an investment opportunity and a performance engine. SWFs are deploying capital into AI initiatives to drive returns while simultaneously embedding AI into risk, portfolio, and investment processes to sharpen performance. And they’re putting a lot of skin in the game: More than $350 billion has been committed to the global AI build-out. Investments cross the entire value chain, including data centers, semiconductors, large language models, and related services, applications, and solutions. Before transitioning to L’Imad, ADQ entered a $25 billion partnership with Energy Capital Partners to develop energy and data center infrastructure in the US, while QIA partnered with Blue Owl to launch a $3 billion data center platform. Roughly 30% of AI allocations are directed toward nation-building initiatives to create domestic champions. Notably, Mubadala and AI holding company G42 co-founded MGX, a $100 billion investment platform focused on AI infrastructure and semiconductors. This reflects Mubadala’s dual ambition for economic diversification and digital sovereignty. PIF signed a memorandum with Qualcomm to establish AI data centers and edge-to-cloud services in Saudi Arabia. Temasek joined the AI Infrastructure Partnership with Microsoft, BlackRock, and MGX to build sovereign-scale data centers across Asia. GIC has also increased its exposure to AI across both public and private markets, backing leading technology platforms and funds globally. Meanwhile, newer funds such as INA are beginning to explore digital infrastructure as part of their long-term investment strategies. AI is also a transformation lever, supercharging SWFs’ internal capabilities. NBIM has become a leader in this space, leveraging AI to streamline investment processes, enhance decision making, and augment internal capabilities—reportedly achieving 20% time savings and near-universal adoption. Similarly, Mubadala has embedded AI into bespoke tools to drive operational excellence. Investment committee members use AI to expedite deal reviews and validate assumptions, while the fund more broadly uses the technology to optimize resource allocation and streamline operations. Funds are also pushing for AI adoption within their portfolio companies, viewing the technology as a core lever for value creation and competitive advantage. Redesigning the operating modelSWFs have evolved far beyond their origins as passive custodians of national wealth. Leading funds are transforming their operating models to match the scale and complexity of the assets they manage today. And modern structures require leaner frameworks, global reach, and governance models that balance speed with control. While technology and data often sit at the center of these new models, there’s no universal blueprint. The ideal form depends on a fund’s specific mandate and asset allocation:

Operating model transformation must also consider these four dimensions:

The next 10 yearsScale is an advantage, but SWFs need long-term vision to ensure their success. SWFs are long-term investors by design, and consistent direction has given them a powerful advantage. To retain that edge in a volatile world, SWFs must commit to sustained execution. If they constantly recalibrate to shifting conditions, they risk drifting off course and reducing their impact. To define a clear path for the next decade, leaders might ask: What does the fund need to become by 2035—and how will it get there? The answers should go beyond AUM or return targets, clarifying ambitions across five dimensions:

The next decade demands strategic clarify and consistency—and bold moves over incremental gains. Tomorrow’s leaders are clarifying their identity today, building capabilities to support it, and executing with discipline. Those who choose a path—and stay the course—will be rewarded. |