Press release

- Payments and lending will continue to be the largest embedded financial services. But these will be bolstered by the growth of adjacent value-added services, including insurance, tax, and accounting.

- Established financial institutions face major challenges from embedded finance and urged to adapt and reinvent business models to take advantage of its opportunities and growing scope

BOSTON— September 13, 2022— Embedded finance, the integration of value-added financial services into software offerings, is set to redefine how consumers and businesses build and manage relationships with financial services, according to new research and analysis from Bain & Company and Bain Capital. The swift acceleration in use of embedded finance, and its transition into the financial mainstream, is being propelled as its proposition enhances customer experience and financial access, alongside cost- and risk-reduction benefits for companies across the value chain.

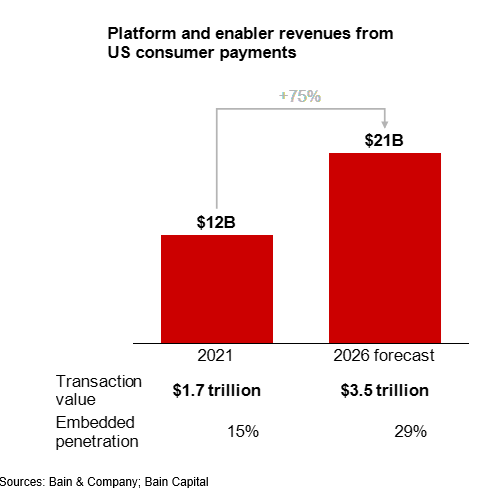

The forecasts for the huge expansion of embedded finance, in a detailed new analysis of the fast-moving sector from Bain & Company and Bain Capital, show that revenue opportunities for software platforms and the enabling infrastructure providers that power these embedded offerings will more than double from $21 billion in 2021 to $51 billion in 2026. The transaction value of embedded finance also will surge $7 trillion in 2026 and account for 10% of US financial transactions.

The factors driving the expansion of embedded finance space and its implications are clear:

Embedded finance can provide a much better value proposition – and platforms are the lynchpin

Businesses and their end customers benefit from contextual, seamless experiences; platforms can unlock new use cases and often use proprietary customer data to improve financial access while reducing costs for their end customers.

Platforms are partnering across the new value chain to deliver these benefits to customers and differentiate their core services. In turn, this increases their ability to spur sales in their core business. For example, embedding payments into the native invoicing workflow improves accounting or business management software for the merchant, significantly reducing time spent reconciling payments and invoices. Embedding financial services helps platforms drive superior economics, increasing customer lifetime value. With minimal incremental customer acquisition costs, platforms can raise average revenues per user, while keeping customers longer.

Market opportunity valued at $51 billion by revenues by 2026, and payments and lending are the largest growth drivers

The forecast jump in revenues will flow from the expansion in transaction volumes and value but also from increasing penetration of embedded finance in specific industries and gains in revenue multiples seen in segments such as business-to-business (B2B) payments as well as in the Buy Now Pay Later (BNPL) market.

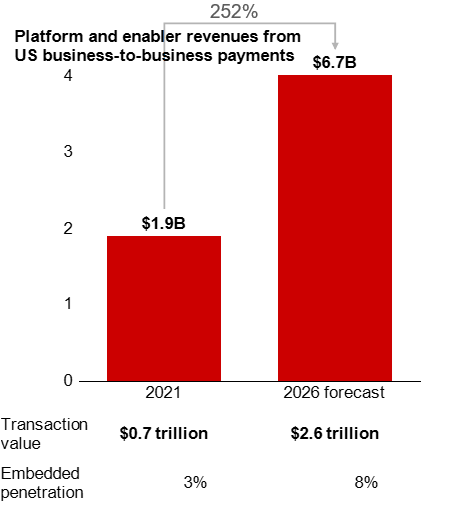

Payments and lending will continue to be the two biggest segments of embedded finance. Currently, consumer payments account for more than 60% of all embedded finance transactions and this is expected to reach $3.5 trillion by 2026. B2B payments have lagged with transactions expected to reach $2.6 trillion by 2026, marking a three-fold increase on levels today. Smaller retail merchants will stand to gain the most from embedded B2B payments, helping these businesses to tackle challenges such as late or unpaid invoices. Embedded finance-driven business lending, meanwhile, is projected to grow five-fold over the next five years, from a mere $200 million in 2021 to $1.3 billion by 2026, thanks to the rise of a range of new specialist providers.

While payments and lending will constitute a significant driver for the rise of embedded finance over the next decade, the analysis also predicts growth in compliance, HR and procurement among a range of areas.

Incumbent institutions confront threats but can realize tremendous growth from reinventing business models

Disruptive digital first organisations, especially platform businesses, are best placed to take advantage of the embedded finance sector’s expansion. Their access to more sophisticated technology, algorithms and data provides them with an edge in finding and targeting the most creditworthy customers. Embedded finance poses a major challenge to traditional financial institutions, threatening to separate banks from their customers and leave them with the low growth, low margin role of a regulated entity. However, there is still a significant opportunity for these institutions to use embedded finance to rethink their core business and drive growth through new services.

Adam Davis, Associate Partner in Bain & Company’s FinTech practice, commented: “Embedded finance has quietly become a significant part of the way consumers and businesses make payments and access funding. In the years to come it will have a transformative effect on the relationship we have with our finances, removing friction from the sector and making financial services more contextual, accessible and helpful. Jeff Tijssen, a Bain & Company expert partner and leader of its global FinTech practice, added: “For businesses this shift is an enormous opportunity. There will be no shortage of growth finance for the sector as platforms experiment with integrating everything from tax to payroll services in the years to come.”

“Embedded finance clearly provides a compelling win-win proposition. For software platforms, these products unlock new revenue streams and for end customers, they routinely increase access to financial services at lower costs compared to traditional financial institutions,” said Blake Adams, a Senior Vice President at Bain Capital. “As one of the longest-tenured investors in the fintech and software spaces, we’ve had the privilege of helping software platforms launch and scale embedded financial offerings while supporting enabled infrastructure players to scale and attain product-market fit. This research clearly signifies that embedded finance is still in its early innings, and we’re excited to support the founders, entrepreneurs, and business leaders who will continue to advance and disrupt this ecosystem,” added Matt Harris, a Partner at Bain Capital.

Media contacts

For any questions or to arrange an interview, please contact:

Bain & Company: Gary Duncan (London) — Tel: +44 (0) 7788 163 791 Email: gary.duncan@bain.com

Bain Capital : Eddie de Sciora (Boston) – Tel: +1 516-458-3783 Email: edesciora@baincapital.com

ベイン・アンド・カンパニーについて

ベイン・アンド・カンパニーは、未来を切り開き、変革を起こそうとしている世界のビジネス・リーダーを支援しているコンサルティングファームです。1973年の創設以来、クライアントの成功をベインの成功指標とし、世界40か国67都市にネットワークを展開しています。クライアントが厳しい競争環境の中でも成長し続け、クライアントと共通の目標に向かって「結果」を出せるように支援しています。私たちは持続可能で優れた結果をより早く提供するために、様々な業界や経営テーマにおける知識を統合し、外部の厳選されたデジタル企業等とも提携しながらクライアントごとにカスタマイズしたコンサルティング活動を行っています。また、教育、人種問題、社会正義、経済発展、環境などの世界が抱える緊急課題に取り組んでいる非営利団体に対し、プロボノコンサルティングサービスを提供することで社会に貢献しています。

商号 : ベイン・アンド・カンパニー・ジャパン・インコーポレイテッド

所在地 : 東京都港区赤坂9-7-1 ミッドタウン・タワー37階

URL : https://www.bain.co.jp