論説

As executives shift gears amid economic worries, they are changing the tools they use to manage their businesses

Global survey results

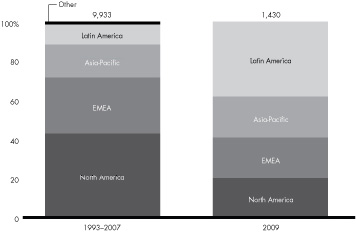

Bain & Company has been conducting global Management Tools and Trends surveys since 1993. Never before have we surveyed executives during a period of such economic turbulence. It is a sign of the times that a cost-cutting tool—Benchmarking—has become the most popular tool for the first time in 11 years. The latest questionnaire was conducted in January 2009 and reflects behavior in 2008. (See figure 1.) It was completed by 1,430 international executives from companies in a broad range of industries and focuses on 25 tools. (See "A history of Bain's Management Tools and Trends Survey," opposite page.) Their answers provide insights into how they think their companies are performing in the downturn and where they believe their organizations ultimately are headed.

To view larger version of this chart

Figure 1: 12 surveys, 9,933 respondents covering a 16-year span

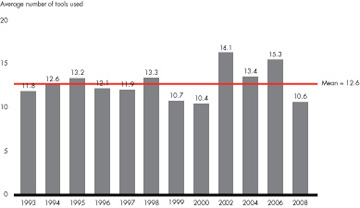

Our recent findings reveal both common themes and distinct differences across regions and industries. Overall, tool use has declined worldwide since 2006. (See figure 2.) Although most executives are primarily worried about successfully tackling short-term financial pressures, they are generally optimistic about the future of their companies. We also found that established economies are much less focused on growth and innovation than emerging economies are; that's especially true in North America, where the emphasis on cost cutting is the strongest.

As an indication of where executives feel their companies are headed, the vast majority—88 percent—of those who downsized in 2008 plan more cuts in 2009. Manufacturers and financial services companies are projected to be the heaviest downsizers. A higher percentage of executives in those industries expect to have significant layoffs in 2009.

To view larger version of this chart

Figure 2: Tool usage dropped dramatically in 2008

Among the other trends to surface: Only 24 percent of executives surveyed believe that the market leaders of today will still be the leaders in five years. We also found that technology and telecommunication companies are the most focused on innovation. And retail and consumer products executives overwhelmingly believe they'll use the recession to improve their competitive position.

Our survey shows that, as executives shift their objectives and priorities, they also are changing the tools they use to manage their businesses. Two cost-cutting-related tools—Benchmarking and Outsourcing—moved up on our Top Ten list. (See figure 3.) Others, like Strategic Planning and Mission and Vision Statements, are heavily used regardless of the economic cycle.

This year's survey found three strong themes.

As the recession intensifies, executives' decisions increasingly are driven by short-term cost-cutting goals. Seven out of 10 executives surveyed say they are worried about how they'll meet their growth targets in 2009, and six out of 10 are planning for a downturn that they expect will last at least until early 2010. That concern is reflected in the increasing popularity of Benchmarking as a way to achieve cost-reduction targets.

While executives-particularly in North America—are heavy users of Benchmarking, they are not uniformly satisfied with the results. The tool landed in the middle of our list for satisfaction. As a sign of the times, Benchmarking knocked out Strategic Planning, now No. 2, which had topped the tool usage list since 1998. Outsourcing also has moved up from seventh to the fourth most-used tool. And Business Process Reengineering, another tool often associated with cost cutting, also is in the top 10.

In follow-up interviews, executives described the battle to contain costs. The vice president of a large insurance company explained, "We're eliminating discretionary investments, and we're off-shoring and outsourcing as much as we can to maintain the lowest possible cost structure. We're concentrating on keeping the legacy systems afloat."

Our survey found that more layoffs are in the cards, even though half of the executives believe that "we should focus more on revenue growth and less on cost reduction." Globally, almost 60 percent of those surveyed expect to make significant layoffs in 2009, almost double the number—34 percent—in 2008. North America is the layoff leader, with 70 percent of the executives planning 2009 layoffs.

Despite the popularity of Downsizing, our research from previous downturns shows that layoffs sometimes come at a heavy cost. In addition to risking the loss of employee support, investors may perceive multiple rounds of layoffs as a symptom of mismanagement and shun the stock. To restore confidence, they need to see a strategy shift to correct problems that necessitated layoffs in the first place.

Not every region is as focused on cost reductions. European and Asian executives are less concerned than their counterparts in North and Latin America about meeting growth targets.

To view larger version of this chart

Figure 3: Top 10 tools

Theme 2: Optimism about future growth

Our survey sheds light on a paradox. Even as executives express deep concerns about their short-term financial outlook, they are voicing optimism about the long term. (See figure 4.) We found that 75 percent of the executives expect to use the recession to improve their competitive position. Since not everyone will end up ahead, such across-the-board optimism seems unrealistic. One executive in the hard-hit financial services sector explained why he's so upbeat: "In the short term, the extent to which our customers are having difficult times reflects on us. But from a long-term perspective, we're very confident. We have the right business model, and even if we lose some customers in the short term, we are confident that we'll win some back in the long term."

Another key finding: many companies are looking hard at ways beyond cost cutting to stabilize their businesses. To help achieve that goal in 2009, executives predict that they'll increase their use of all 25 management tools in our survey. Tools that promote growth are expected to have the biggest gains.

"We're using this downturn as an opportunity to aggressively pursue our customers and understand their needs and business drivers," said the director of a telecommunications company that is using deeper customer insights to spur both growth and customer loyalty. "We're focusing on relationships, tailoring our solutions to customers' needs and providing superior service."

Although we've learned from previous surveys that tool use rarely increases as much as executives anticipate, the responses provide insights into their objectives. For example, only 10 percent now use Decision Rights Tools—a systematic way for organizations to make key operating decisions and put them into action. But 39 percent of the executives say they plan to use the tool this year.

What this tells us is that even as they struggle through the worst downturn in their experience, many executives are recognizing the need to continue developing capabilities like innovation and organizational effectiveness in lockstep with trimming their ranks.

To view larger version of this chart

Figure 4: Executives express strong concerns and surprising long-term optimism

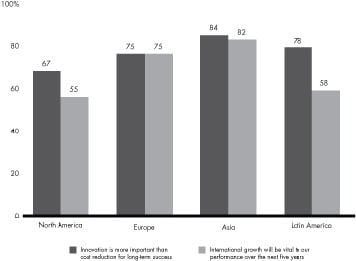

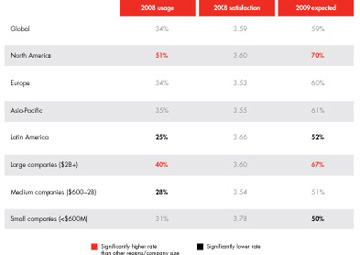

As they look to the future, our survey found wide regional variation among respondents' expectations regarding international growth. When asked if international growth will be vital to their performance over the next five years, 82 percent of Asian respondents agreed. That compares with 75 percent in Europe, 58 percent in Latin America and 55 percent in North America. (See figure 5.)

Innovation is another test of a company's focus on growth. (See figure 5.) Globally, two of the five tools with the largest projected jump in use between 2008 and 2009 are Voice of the Customer Innovation and Collaborative Innovation. Asian companies expressed the strongest commitment to innovation. While still heavily using tools like Downsizing to contain costs, 84 percent of Asians surveyed agreed that "innovation is more important than cost reduction for long-term success," followed by Latin America (78 percent) and Europe (75 percent). North America trailed with just 67 percent. And two-thirds of Asian managers said that "we could dramatically boost innovation by collaborating with other companies."

To view larger version of this chart

Figure 5: North Americans are less focused on innovation and international growth than rest of the world

Theme 3: Confidence in India and Latin America

Despite the global downturn, confidence remained relatively high among executives in India and Latin America when we surveyed them in January, even as projections for GDP growth dropped in both places. Executives in China, who felt the pains of the downturn earlier, appeared less confident.

When asked if they are planning for the downturn to last until early 2010, a full 70 percent of the Chinese executives agreed, compared with only 56 percent of the Indian respondents. This difference is underscored by downsizing plans for 2009–40 percent at Chinese firms say they will have significant layoffs, but just 23 percent of Indian respondents expect significant layoffs.

Indian and Latin American executives also are less critical of company management—almost two-thirds of the Chinese respondents believe that unclear decision-making authority is hurting their performance, in contrast to less than half of the Indian and Latin American executives. Finally, the overwhelming majority of Indian and Latin American managers say they'll use the recession to improve their competitive position, while Chinese companies are somewhat less confident.

Latin American companies' focus on growth is apparent in their tool choices. They are most likely to use Strategic Planning and Growth Strategy Tools in 2009.

In Asia-Pacific, we found some distinct differences in how tools are used throughout the region:

- Chinese companies use Benchmarking, Strategic Planning, Supply Chain Management and Total Quality Management more than their counterparts elsewhere in Asia;

- Fewer Indian companies use Customer Segmentation, the sixth most-popular tool, globally;

- Indian companies are more satisfied with four tools than other firms throughout the Asia-Pacific region: Core Competencies, Benchmarking, Strategic Alliances and Collaborative Innovation.

The big picture: Tool use and satisfaction

The global downturn definitely has taken a toll on management tool use in 2008, both in the number and kinds of tools executives used. Worldwide, tool usage declined, with firms employing an average of 11 tools, down from 15 in 2006. The drop suggests that companies held off on launching new initiatives or took a wait-and-see approach before refocusing efforts. As we found in the past, the larger the company, the more tools are used. However, last year, even usage among large companies dropped dramatically.

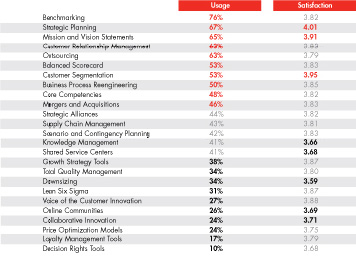

Some tools stand out as winners, and some as losers. (See figure 6.) Three tools were above average in both use and satisfaction: Strategic Planning, Customer Segmentation and Mission and Vision Statements, all of which help guide management's thinking on strategic issues, especially during times of significant change. In contrast, tools with below-average usage and satisfaction include two newer tools—Online Communities and Collaborative Innovation—as well as Downsizing, even though executives said they plan to increase layoffs in 2009.

One executive described Downsizing as a dual-edged sword that requires weighing the potentially negative effects on the workforce against immediate cost pressures. "When layoffs affect the fundamental labor team-management and long-term labor—that's when it most hurts morale," said the vice president of a group of car rental companies. "The pain of those layoffs is felt throughout the organization, and people don't forget it. But we have to be respectful of the business and make sure our cost structure is in line."

As we've found in past surveys, companies get the best results when they employ tools as part of a broad initiative, instead of on limited projects. For example, Lean Six Sigma is the top-ranked tool in satisfaction when part of a major effort. But it ranks 24th when used on a limited basis. The findings suggest that executives should consider the relative benefits of major vs. minor efforts before deciding which tools to use and how much to invest in an initiative.

To view larger version of this chart

Figure 6: Usage and satisfaction rates in 2008

Top 10 tools

The global downturn has re-ordered the Top Ten list of most used tools, reflecting fast-changing executive priorities and goals. Two tools that moved up the global Top Ten are related to cost cutting-Benchmarking and Outsourcing. As executives focused less on the long term, Strategic Planning—the perennial number-one most-used tool—fell to second place.

One executive observed that for Benchmarking to be most effective, his company has to dig deeper: "I'd like to see more granular, actionable benchmarking in the future. That way if we're not doing well compared to our competitors, it's a red flag to address a problem."

As we've mentioned, while overall tool use dropped in 2008, especially for long-term planning, this is expected to change in 2009. Executives are projecting a large increase, particularly among growth and innovation-related tools.

One reason for the projected increase in innovation tools: the need for firms to differentiate themselves as competition intensifies. "We've pulled a lot of innovation triggers already," says the rental car executive. "But if the economic environment hits our industry harder than we currently anticipate, we will focus more on innovation to survive."

Plans to increase the use of specific tools highlight what executives think is important—even if projections fall short. An increase in the use of Scenario and Contingency Planning suggests that companies are starting to search for innovative ways to remain competitive and emerge from the downturn in a stronger position, even as they're uncertain about the severity or how long it will last. Tools like Price Optimization support both short-term gains and long-term growth by pinpointing prices that cash-strapped consumers can afford and are willing to pay—while also protecting profit margins.

While tool use is similar around the world, there are distinct differences when we break out the Top Ten tools by region. As we've mentioned, Downsizing was much more widely used in North America. (See figure 7.) And, as we've found in past surveys, so is Strategic Alliances—suggesting that North American executives are more comfortable with alliances than executives in other regions.

European executives used some popular tools less in 2008 than their global counterparts did. They include two tools focused on working with other companies—Outsourcing and Strategic Alliances—and two strategy-related tools—Strategic Planning and Growth Strategy Tools. That may reflect the fact that, at the time of the survey in January 2009, European executives were unsure about how the downturn would affect them or when it would hit.

In contrast, strategy was key for Latin American companies. They used both Strategic Planning and Growth Strategy Tools significantly more than other regions. Latin American companies also downsized less, although they were the heaviest users of Outsourcing.

In Asia-Pacific, Chinese executives have embraced four cost-management and planning tools: Benchmarking, Strategic Planning, Supply Chain Management and Total Quality Management.

To view larger version of this chart

Figure 7: All regions expect to increase downsizing in 2009

Our survey respondents represented the full spectrum of industries. While the top 10 tools are similar across industries, we found variations that underscore how the global downturn is affecting sectors differently.

By industry, the heaviest tool users are:

- Consumer products

- Pharmaceuticals and Biotech

- Food and Beverage

- Chemicals and Metals

By industry, the lightest users are:

- Utilities and Energy

- Construction and Real Estate

- Retail

- Financial services

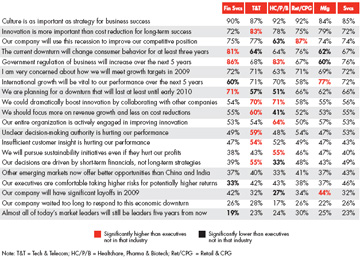

Financial services executives have the most pessimistic economic outlook of all sectors surveyed. (See figure 8.) In greater numbers than any other industry, they are planning for a downturn that will last until early 2010. They also are strong believers that the downturn will affect consumer behavior for at least three years. And they are the biggest users of Downsizing—70 percent said that they downsized in 2008 or are likely to do so again in 2009. One insurance executive described being caught between short- and long-term pressures: "In the long term, unless we come up with tools that allow us to position ourselves as a leader of the industry and achieve growth potential, we cannot differentiate ourselves and state our value. But right now, client retention is more important than growth."

To view larger version of this chart

Figure 8: Financial services executives expect changes across the board-from customers, the government and competitors

Technology and telecom executives are the least concerned about the long-term impact of the recession. (See figure 8.) They are the most focused on innovation. In fact, seven out of 10 believe that they could dramatically boost innovation by collaborating with other companies. "We would consider collaborating with competitors if necessary," said one telecommunications executive, "but there would have to be legal protection on both sides." They also are the most concerned that current management is hurting performance with unclear decision making and insufficient customer insight. Their tools choices reflect these technology and telecom firms' priorities. While all other industries rated Benchmarking as their most-used tool, technology and telecom executives named Customer Relationship Management as key. Strategic Alliances and Knowledge Management also are among this sector's top 10.

Healthcare, pharmaceutical and biotech may be the safest industries to be employed in for the short term. (See figure 8.) Fewer executives in these industries predict they will have significant layoffs in 2009. Three tools are used more by these companies than other industries: Outsourcing, Core Competencies and Lean Six Sigma.

Many retail and consumer product goods (CPG) executives are overwhelmingly optimistic about the recession's long-term impact. (See figure 8.) Almost nine out of 10 believe that their companies will use the recession to improve their competitive position. Since not everyone will emerge winners, this optimism may be unrealistic. Their tool choices show an emphasis on cost cutting to help offset declining consumer demand. As in most other industries, Benchmarking is the most popular tool. Supply Chain Management—a tool aimed at squeezing costs through efficiency—is the second most-used tool by retail and CPG firms.

Manufacturing firms are more focused than their counterparts in other industries on international growth. Almost eight of 10 executives agreed with the statement "International growth will be vital to our performance over the next five years." They also are the most likely to have significant layoffs in 2009. They employ the following cost-reduction and efficiency-related tools more than other companies: Balanced Scorecards, Supply Chain Management, Total Quality Management and Lean Six Sigma.

Sidebar/intro

A history of Bain's Management Tools and Trends Survey

Starting in 1993, Bain & Company has surveyed executives around the world about the management tools they use and how effectively those tools have performed. We focus on 25 tools, honing the list each year. To be included in our survey, the tools need to be relevant to senior management, topical and measurable. By tracking which tools companies are using, under what circumstances and how satisfied managers are with the results, we've been able to help them make better choices in selecting, implementing and integrating the tools to improve their performance.

With this, our 12th survey, we now have a database of nearly 10,000 respondents and can systematically trace the effectiveness of management tools over the years. As part of our survey, we also ask executives for their opinions on a range of important business issues. As a result, we are able to track and report on changing management priorities.

For a full definition of the 25 tools, along with a bibliographical guide to resources on each one, please see the Bain & Company booklet: Management Tools 2009: An Executive's Guide.

Darrell Rigby, a partner with Bain & Company and leader of Bain's Global Retail and Global Innovation practices, has conducted Bain's Management Tools and Trends survey since 1993. Rigby is also author of Winning in Turbulence, published by Harvard Business Publishing. Barbara Bilodeau is director of Bain's Customer Insights Group.

Copyright © 2009 Bain & Company, Inc. All rights reserved.

Editorial team: David Diamond and Elaine Cummings

Layout: Global Design

First published in 5月 2009